|

|

|

Happy new year! You’re receiving Vested Interest, our newsletter about what the latest economic news might mean for your money, career, and life in general. Get in touch via askwealthfront@wealthfront.com with comments and questions.

|

|

|

|

|

|

- An intriguing idea for bringing Chinese EVs to the US

- The obesity-drug stock price roller coaster

- A glossary of obscure Industry jargon words like “axe” and “hedge fund”

- What if data center spending isn’t out of control after all?

|

|

|

|

|

|

Meta’s rendering of its proposed Louisiana data center.

|

|

|

|

|

Three numbers that explain the economic moment.

|

|

|

11%

|

|

The gap in performance between the MSCI Emerging Markets Index and the S&P 500 thus far in 2026. In other words: As of right now, US stocks are in the red for the year, while stocks in countries ranging from Brazil to the United Arab Emirates are not. (Information in this newsletter is accurate as of publication time but is subject to change.) We get more into the domestic part of that equation below, but abroad there’s something of a rubber-band regression at work. The out-performance of the Magnificent 7 in recent years meant portfolios were increasingly dominated by American equities, and rebalancing them means taking money out of the US and putting it in places whose companies have come to seem relatively cheap. Some investors, meanwhile, are selling portions of their US assets as a “hedge” against the potential volatility created by geopolitical tension and threats to Federal Reserve independence. One practical consequence of all of this? American dollars themselves are in less demand than they used to be—the ol’ greenback is worth about 8% less relative to other currencies than it was a year ago.

|

|

|

|

122%

|

|

The current tariff imposed by the US on Chinese electric vehicles—an all-but-official ban that Ford CEO Jim Farley reportedly suggested circumventing in a recent conversation with several Cabinet officials. Farley’s pitch, according to Bloomberg, was not to drop the tariff, but to let China’s surging automakers build cars in the US at factories that would be built and operated jointly with American incumbents. It’d be a mirror image of the tactic China used to gin up a competitive auto industry in the first place, which was to let foreign carmakers into Chinese markets through ventures that shared intellectual property and profits. Whether this will finally lead to Americans getting behind the wheel of BYD’s world-leading EVs, though, is still TBD: Among other things, modern cars are stuffed with technology that can be used for remote surveillance, which means that both industrial policy and national security concerns will have to be worked through before anything becomes law.

|

|

|

|

3

|

|

How many years PlayStation fans reportedly might have to wait—i.e. until 2029—for the company’s next-generation PlayStation 6 thanks to a shortage of computer memory. (Sony’s initial rumored target for releasing the console was 2027.) Dynamic random access memory (DRAM) is the workhorse of consumer computing, keeping track of information that processors need close at hand to do stuff like generating graphics. But other types of RAM are required in AI data centers, and manufacturers have shifted their attention away from the at-home stuff; the resulting scarcity has driven up the price of DRAM by at least 80% this year, per one estimate. That will have repercussions across the world of consumer electronics, but gamers, naturally, are already creating strategy guides for how to maximize power in a world of memory shortages.

|

|

|

|

|

Ups and downs in the Ozempeconomy

|

|

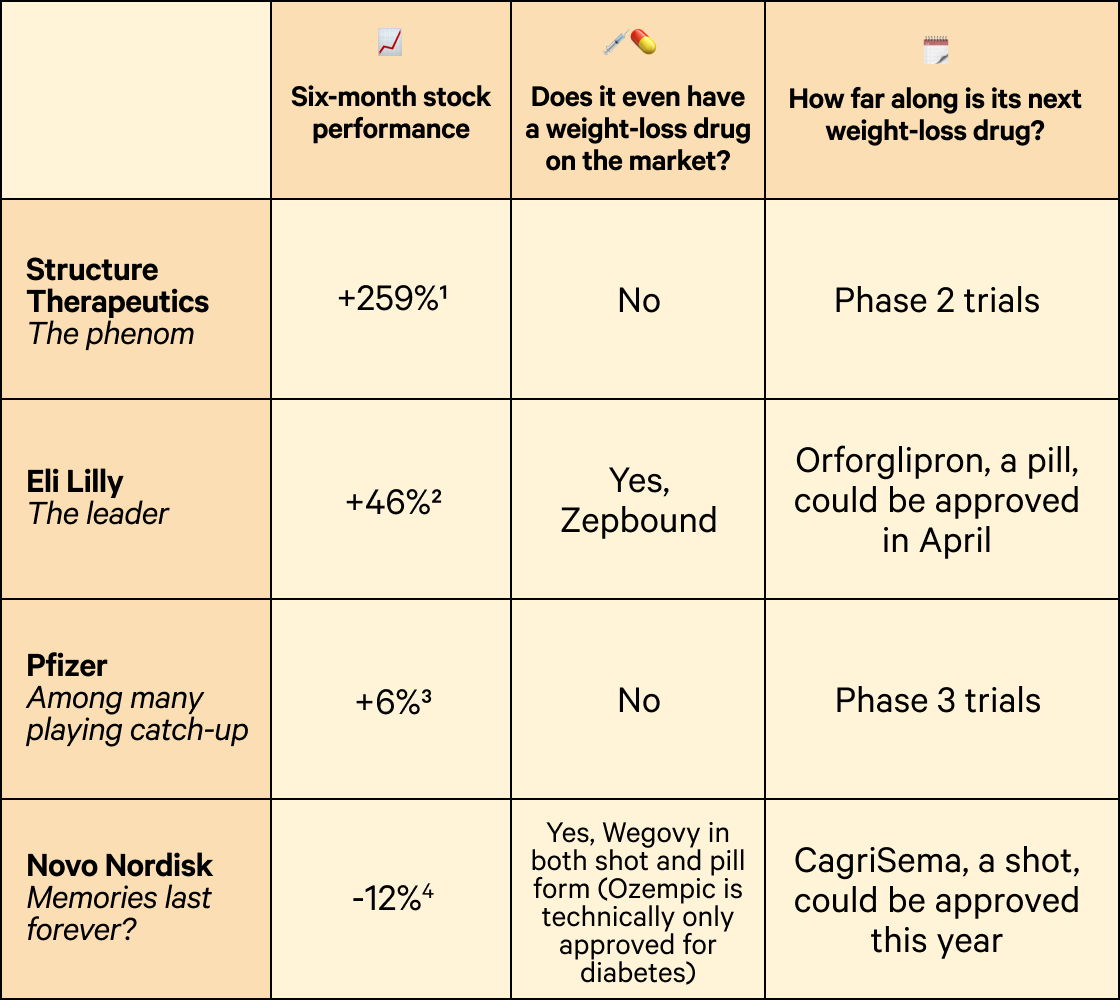

Big pharma’s obesity-drug era illustrates the maxim that beliefs about future profits, not present-day earnings or brand awareness, are what drive stock prices. While Novo Nordisk may have invented the treatment that’s now synonymous with weight loss, recent valuation trends indicate that investors frankly couldn’t care less—and that they’re looking instead at the industry’s pipeline of treatments that might work just as well or better than existing meds while being taken less frequently and inducing fewer side effects. (In this world, “vomiting rate” is a key metric.)

|

|

Note: Three trial phases, which can take years, must be completed before a drug is submitted for FDA approval.

|

|

|

1The 218-employee company’s stock has surged as the eyebrow-raising efficacy of its developmental GLP-1 pill has made it a likely acquisition target.

2Overtook Novo Nordisk, and now claims 58% of current market share, after introducing a drug that targets two different types of hormone receptor. Next up: A shot that targets three receptors.

3One of several industry behemoths still trying to get in the game—we could have put Roche or Amgen in this spot too. Had to abandon its own GLP-1 effort in April 2025 over liver-damage concerns, but gained access to a trial-stage drug that only needs to be injected once a month by acquiring Metsera in a high-profile bidding war.

4Revenue has been battered by price wars, and it lost the battle for Metsera. Its own two-hormone effort, CagriSema, shows promise in trials.

|

|

Thanks to Evan David Seigerman of BMO Capital Markets and Karen Andersen of Morningstar for sharing their insight into the sector. Stock investing includes risks, including fluctuating prices and loss of principal.

|

|

|

|

|

What they’re talking about in Industry

|

|

|

|

|

|

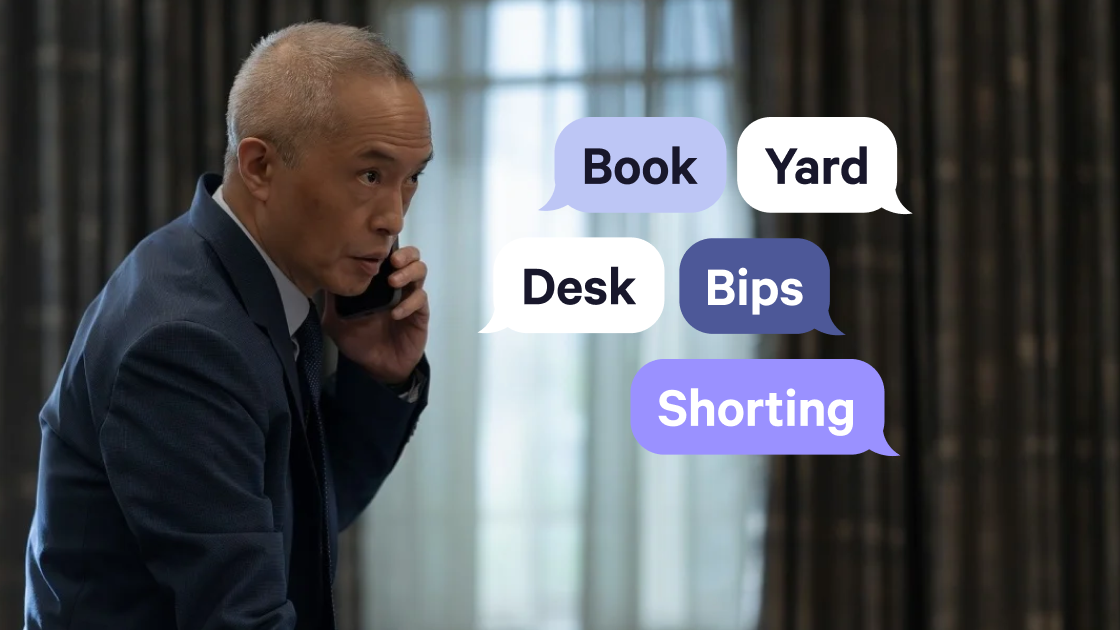

Season 4 of HBO’s hit London finance drama wraps up March 1. Here, a speed run through the show’s most commonly used jargon, from least to most insider-y. (They claim they’re trying to make the dialogue more accessible, by the way.)

Desk: Team within a bank or fund that specializes in a particular asset type.

Hedge fund: Fund for accredited (read: wealthy) investors whose name refers to the strategy of “hedging” high-risk bets with short positions, although in practice they often don’t follow that strategy (and often fail to make much money).

Shorting: Borrowing an asset that you think is overrated, selling it, and buying it back later at a (hopefully) lower price to return to the broker you borrowed it from. Screenwriters love the tension that shorting creates, but it’s gotten a lot harder to do in real life recently.

Bips: Basis points or bps, i.e. one-hundredths of a percentage point. For example: 25 bps = 0.25%.

Spread: The difference between two related financial figures. The spread between government bond and corporate bond interest rates, for instance, is notably tight right now.

Vol: Volatility, or the rate at which a price fluctuates. Higher vol = higher risk.

Book: Short in this case for “trading book,” or the current positions a given manager has taken on certain assets.

Yard: A billion units of a given currency.

Half a yard: C’mon, you can do this.

Axe: Short for “axe to grind,” i.e. a trader’s motivation for buying or selling a specific security, which they might want to keep to themselves so others don’t take advantage of it. Also the nickname of the main character in a different TV finance melodrama, which that show’s fans think is a reference to a pioneering theorist in the field of high-stakes decision making.

|

|

|

|

|

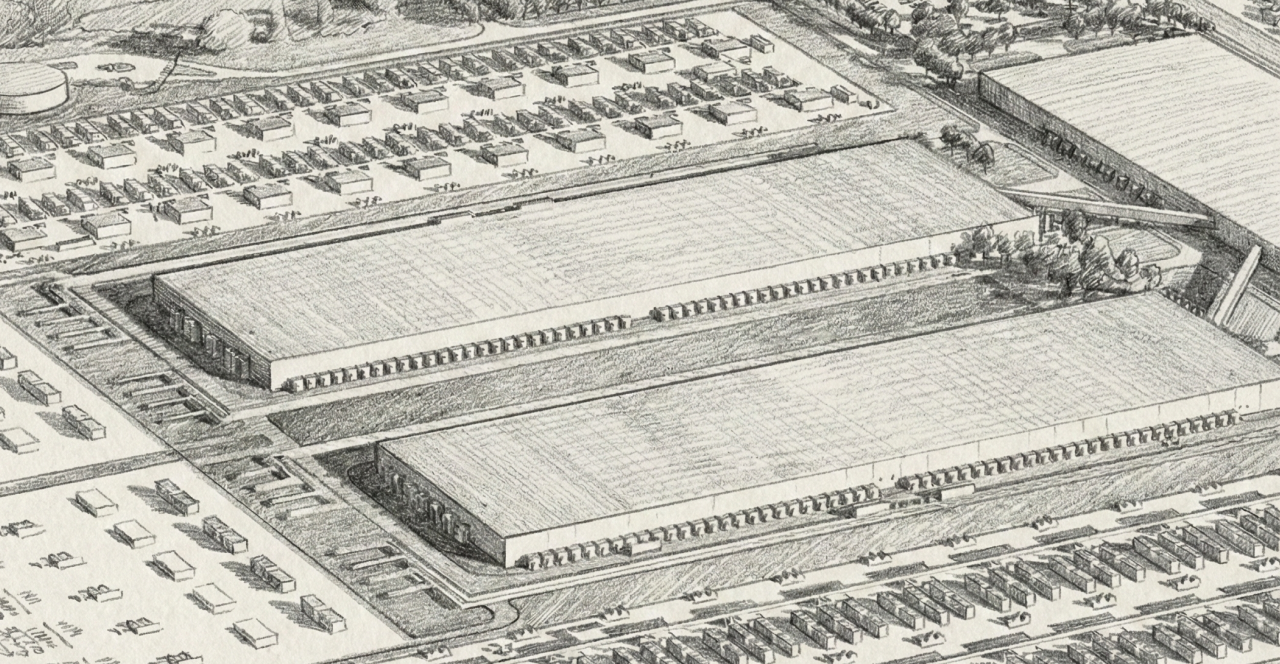

How a very large construction site in Louisiana encapsulates the debate over AI spending

|

|

|

|

|

The Big Short has been getting brought up a lot recently. (Image: Paramount Pictures.)

|

|

Big tech companies have had a rocky year so far—and one of the reasons why, headlines say, is that they’ve been announcing so many enormous financial commitments to AI data centers. Those same kinds of announcements, though, used to make tech stocks go up. What gives?

In short, concerns about the size of AI-related debt have crept from the edges of the worldwide financial conversation to its center. One particular type of debt, and in fact one particular debt deal involving Meta and the state of Louisiana, is often cited to exemplify these concerns. So let’s dig into it!

The basics

Tech giants like Meta are racing to develop more advanced LLMs and AI agents, but even they don’t want to use their cash flow to pay up front for the enormous data centers required to do so. So they’re finding other sources of funding and spreading some risk around. Meta, for instance, will be working through a so-called “special purpose vehicle” (SPV) to build an especially huge data center—the construction site takes up five square miles—in northeast Louisiana. The SPV, named Beignet, will raise some $30 billion from investors and own the resulting facility and computers. If things go according to plan, Beignet will pay investors back using money Meta has legally promised to give it in rent or other payments. Other data centers around the country are being built via SPVs, too, while some are being financed via “asset-backed securities” through which investors can buy claims on pieces of various data center rent streams.

The skeptical case

Why does this make some people nervous? Well, as it happens, SPVs and sliced-and-diced real-estate securities both helped cause the 2008 financial crisis. In the years leading up to the collapse, Wall Street banks surreptitiously dumped ill-advised loans into SPVs to make their own books look cleaner; an overlapping set of bad actors was busy bundling high-risk subprime mortgages into asset-backed securities that were sold to investors who didn’t understand what they were getting. Eventually, it all blew up.

And guess who else used SPVs to hide debt? Enron, an energy company that was also involved in ill-advised bets on dot-com-era technology! You can see the argument: AI debt potentially combines the frenzy for investing in tech infrastructure that defined the dot-com crash, the securitization of speculative real estate assets that defined the Great Financial Crisis, and the creative accounting that paved the way to both.

The devil’s advocate case

There’s a famous line in finance about stock market downturns predicting nine of the last five recessions. The point of the saying is this: One situation can look a lot like another without ending the same way. In the case of SPVs and AI, similarities to the circumstances that preceded past crises could be obscuring key differences.

For one, very few people knew about the SPVs involved in the crashes described above until afterward because they were designed to hide information. The creation of Meta’s SPV, and the bet on AI’s potential that underlies it, was a landmark deal that the company wanted the market to notice. It’s also not inherently suspicious that a business would seek out partners in a complicated, expensive project outside its core area of expertise.

In this view, the scope of projects like Meta’s might be extraordinary, but their potential rewards are considerable, and their structure—in which outside entities take on risk and responsibility in exchange for a long-term financial commitment from a company with well-established revenue streams—is appropriate to the task. Also, for what it’s worth, creating an asset-backed security by loaning money to one of the world’s largest tech companies seems like more honest work than creating an asset-backed security by giving a mortgage to someone with bad credit and using their home as collateral.

The strategic middle ground

So, will data centers pay for themselves in the long run? One recent attempt to answer the question empirically found reasons to be skeptical alongside reasons to be optimistic—and noted that in buildout races of this sort, some projects can succeed and consolidate the available market while others never even end up being completed. (The concept of the productive bubble is related.) Discussion of AI tends to focus on the most extreme potential outcomes: The creation of tools powerful enough to reshape society, or a collapse that’s remembered like tulip mania. But there’s a wide range of possibilities between those poles, and the long-term history of the stock market suggests that the most prudent position when it comes to companies attempting ambitious growth is to be prepared for any of them.

|

|

|

|

|

|

# of mentions of AI in this issue 7

# of mentions of crypto in this issue 0

# of mentions of vomit rate in this issue 1

|

|

|

|

|

|

| Wealthfront Corporation, 261 Hamilton Ave. Palo Alto, California, 94301, US

|

The content provided in this newsletter is for informational and educational purposes only and does not constitute investment advice or a recommendation of any particular security, strategy, or account type. Views expressed are as of the issue date, based on the information available at that time, and may change based on market or other conditions. The content does not purport to be a complete description of the securities, markets, or developments referenced herein. The information has been obtained from sources considered to be reliable, but we do not guarantee its accuracy or completeness.

The Standard & Poor’s 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The MSCI EM (Emerging Markets) Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of the emerging market countries of the Americas, Europe, the Middle East, Africa and Asia. The MSCI EM Index consists of the following emerging market country indices: Brazil, Chile, Colombia, Mexico, Peru, Czech Republic, Egypt, Greece, Hungary, Poland, Qatar, Russia, South Africa.Turkey, United Arab Emirates, China, India, Indonesia, Korea, Malaysia, Philippines, Taiwan, and Thailand.

All indices are unmanaged and may not be invested into directly.

The information contained in this communication is provided for general informational purposes only, and should not be construed as investment or tax advice. Nothing in this communication should be construed as a solicitation, offer, or recommendation, to buy or sell any security. Any links provided to other server sites are offered as a matter of convenience and are not intended to imply that Wealthfront Advisers or its affiliates endorses, sponsors, promotes and/or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Please see our Full Disclosure for important details.

Investment management and advisory services are provided by Wealthfront Advisers LLC (“Wealthfront Advisers”), an SEC-registered investment adviser, and brokerage related products are provided by Wealthfront Brokerage LLC ("Wealthfront Brokerage"), a Member of FINRA/SIPC.

Wealthfront Advisers and Wealthfront Brokerage are wholly-owned subsidiaries of Wealthfront Corporation.

|

|

|

|