|

|

| Issue #7 ⇒ |

April 17, 2026 |

|

|

|

- Markets unfazed by data center backlash, global impact of war

- How Iranian missiles crippled part of the supply chain for airplanes and tinfoil

- BYD vs. Tesla vs. big pickup trucks

- The science of spending too much money even when you are really, honestly trying to be responsible

In our last issue, we tried to figure out what Europe’s whole deal is, or at least why its stock indexes are doing what they’re doing. Read it here.

|

|

|

|

|

| Things to spend money on—they can really creep up on you! Pool photo by Aleksei Toropov via stocksy, oysters from Unsplash. |

|

|

|

| Three numbers that explain the economic moment. |

|

| 12 |

|

The number of states whose legislatures have considered a moratorium on data-center projects, per the Wall Street Journal; on Monday, Maine became the first to pass one. Meanwhile, Bloomberg reports that half of the data centers meant to go live in 2026 may be delayed or canceled because electrical parts are in short supply. For now, at least, the market is not sweating it; in fact, the S&P 500® is now higher than it was before the war in Iran started. (Information in this newsletter was accurate as of the time of writing but is subject to change.) Collectively, in other words, investors still think the fighting and blockading will be wrapping up soon and the AI computing hubs that do get built will still drive a lot of growth.

|

| |

| 14℃ (57℉) |

|

Roughly speaking, that’s the average daily temperature in countries that seem to do the best at soccer—at least according to the predictive model developed by Joachim Klement, a UK-based investment analyst whose system has correctly forecast the outcome of every FIFA World Cup since 2014. Funny story: Klement actually launched his project to make a point about how unreliable oversimplified models can be. Unfortunately for the cause of convincing people not to throw away money on sports predictions, he keeps getting it right—so now says he considers his work “a study in how people fall for forecasters who have no skill but are exceedingly lucky.” (One place global instability does seem to be dampening demand, by the way, is the World Cup hotel room market.)

|

| |

| 32% to 56%

|

|

The portion of cryptocurrency holders who report gains to the IRS, as estimated by the authors of a recent article in the Review of Accounting Studies that compared 2013-2021 tax filing data with other research into rates of crypto ownership in the US.

|

|

|

|

|

|

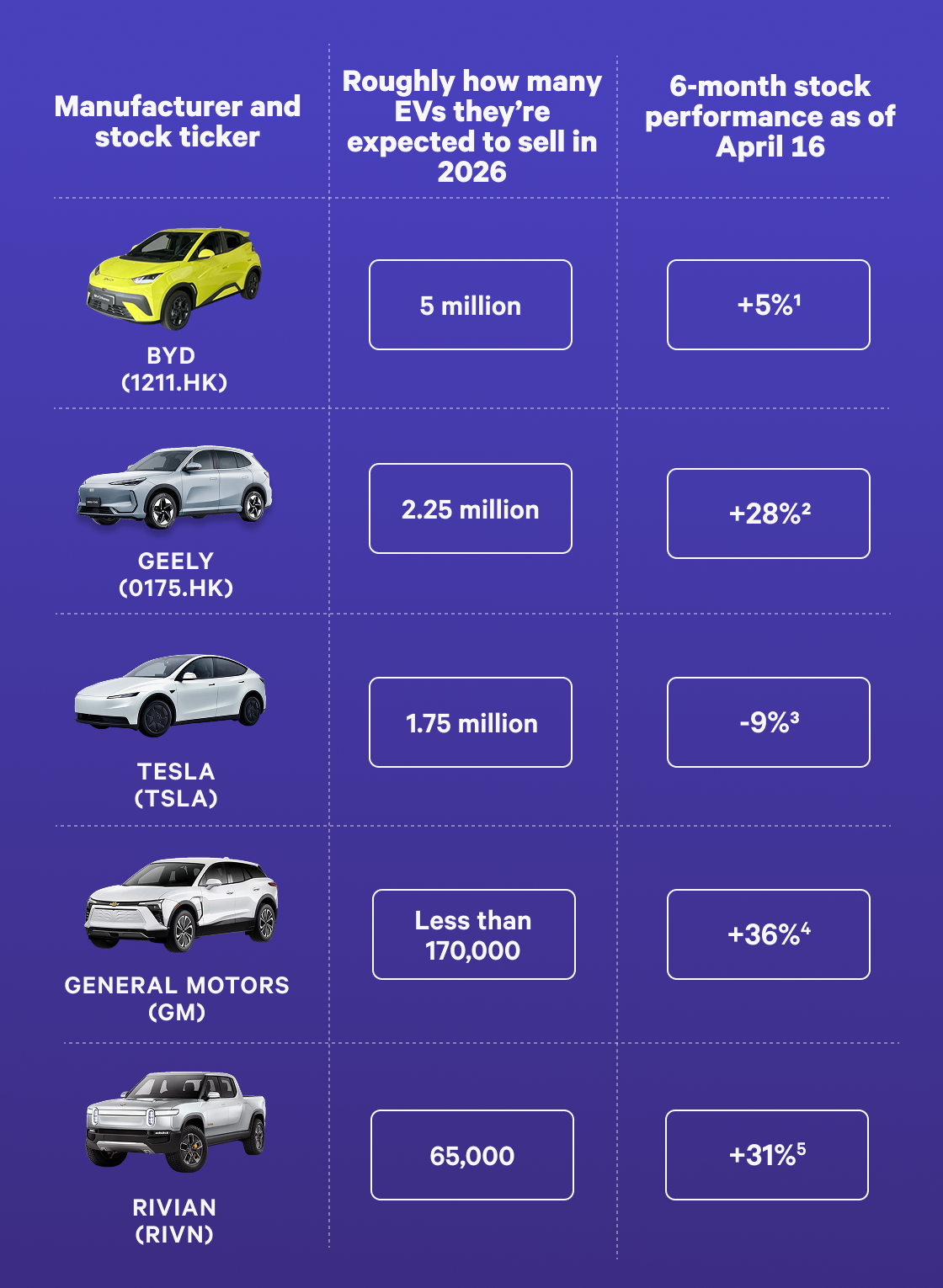

| It’s a good time to be selling electric vehicles … mostly |

|

|

Electricity seems especially likely right now to be the long-term future of vehicular transportation. At the same time, EV sales in the US have fallen off, the world’s leading EV maker is in a domestic price war, and the European and Asian consumers who buy most EVs are threatened by Iran fallout. Here, a rundown of how the major players (and one notable ex-major player) in the market have been doing.

|

|

| Sales estimates via Morningstar, Geely guidance, Tesla analyst consensus, VW guidance referring to 2025 figures, GM guidance referring to 2025 figures, and Rivian guidance. Stock data from Bloomberg. |

1Intra-China price wars between brands had investors concerned, but BYD’s overseas sales jumped 65% in March amid the ongoing Iran oil shock. (We’ve listed the ticker abbreviation for the company’s Hong Kong shares.)

2China’s Geely has surged on plausible ambitions to become one of the world’s top five automakers by 2030.

3Tesla’s polarizing CEO has turned off some potential buyers, though he’s managed to continue attracting some investors with plans to pivot the company to humanoid AI robots.

4GM’s decision to wind down most EV production and instead focus on something more familiar to its legacy—big gas-powered trucks—has gone over well.

5Rivian cut about 600 jobs in late 2025, but a profitable fourth quarter and the upcoming launch of its R2 model look to be helping.

Securities shown are for informational purposes only, not a recommendation to buy or hold. Past performance does not guarantee future results.

|

|

|

|

|

|

| How factories work, or don’t, in wartime |

|

|

|

|

|

Above: A 2022 photo of a “smelting potline” taken at the Emirates Global Aluminum plant in Abu Dhabi that was damaged by an Iranian missile strike last month. Global aluminum prices rose two percent just on the news that this single site had been forced into an “uncontrolled shutdown.”

The potlines use electrolysis to isolate pure aluminum from ore; each of the handful of lines at a major factory might contain hundreds of steel, ceramic, and carbon “pots.” During a sudden shutdown, the molten material inside all those pots is liable to solidify, requiring lengthy repairs. EGA has announced that recovering from the attack could take a year, and products ranging from kitchen foil to airplanes and laptops could soon be paying the price.

Our thanks to David Gildemeister, an associate professor of materials engineering at Purdue University, for educating us on the aluminum smelting process.

|

|

|

|

|

|

| Introducing the concept of fun-related cost creep—and how to deal with it |

|

|

|

|

|

It’s a common problem: You budget a certain amount for a richly deserved night on the town. (Or perhaps a richly deserved weekend trip packed with wholesome family fun. Not everyone is in the same life stage!) But you forget about the cost of coat check, transportation home, and late-night pizza (or the cost of parking a Honda Pilot, providing three meals a day for children, and buying plastic souvenirs at the zoo). You end up spending twice as much as you planned, even though you’d planned responsibly for the cost of the centerpiece dinner, hotel room, or zoo package.

We’re trying to make “frick” happen

We call this fun-related cost creep, or FRCC, a.k.a. “frick”—and although we admit we made that term up in the hopes that it would go viral and make us popular, personal finance professionals think we’re on to something. “We think about the big things when it comes to fun,” says HerMoney founder and former Today show financial editor Jean Chatzky—like plane tickets and hotel costs. “All of the ancillary things that go along with the fun are very often forgotten.”

It’s science!

There’s actually academic research into why this happens, which we spoke about with Ray Charles "Chuck" Howard, an associate professor at the University of Virginia’s Darden School of Business and an expert on the psychology of financial decision-making. In short, when we think about potential future expenses, our brains are inclined to remember normal, regular transactions—modal costs, to put it in mathematical terms, like utilities and rent or mortgage payments. We don’t do as well in predicting one-offs like repairs or doctor bills (or coat check and zoo souvenirs) that contribute to our mean spending. This makes sense on some level: Unpredictable expenses are, individually, unpredictable. But over the long run, something always comes up.

“The human mind is not very good at coming up with atypical outcomes,” says Howard. That, he says, is why “budgets are an imperfect way to control impulse and atypical purchases.”

Howard also notes what he calls the “what the hell effect,” a common-sense concept that has been validated in research on dieting. Eating one cookie, for example, often leads people to eat a second and a third because they reason that if they’ve already broken their self-imposed rules, they’ve got nothing else to lose. The psychology of spending is similar, Howard says. “If you're already dropping a bunch of cash on a hotel and fancy dinner, you might be inclined to think ‘what the hell, I might as well get bottle service at the club too.’”

Salad-related macro context

Chatzky notes that many people’s mental budgets probably haven’t fully adapted to five years of higher-than-normal inflation. “If we haven't accepted or realized that the prices of things have gone up, we probably haven't done the reverse calculus, which is, unless my salary has grown by that much too, I can’t afford as much as I used to.” It's a trap even personal finance experts fall victim to. A few months ago, Chatzky was shocked to find herself spending more than $20 on a salad while traveling. “I think a lot of us don't want to accept yet that that is how much a salad at the airport costs,” she says.

FRCC, the brain, and you

The good news: Howard has also found that even setting an optimistic budget—one you end up exceeding—is financially useful. In a 2023 study, he and a co-author (Marcel Lukas of St Andrews University in Scotland) analyzed more than 350 million transactions made by users of a UK personal finance app and found that setting overly ambitious budgets led to a 21.9% reduction in spending compared to not budgeting at all.

He gives the example of setting a monthly limit of $500 for entertainment spending but exceeding it by $250. “Most people look at that and think: I’ve failed,” he says. “But in reality, most people in this situation were probably spending more than $750 before they set a budget.” Research he co-authored has also found that making a conscious effort to envision unusual one-off costs makes spending forecasts more accurate. In other words, applying the principles of mindfulness to the “what the hell effect” and the price of salad could be beneficial. Even if we do succeed in making “frick” happen, it doesn’t have to happen to you.

|

|

|

|

|

|

# of mentions of AI in this issue: 2

# of mentions of crypto in this issue: 2

# of mentions of a guy named Ray Charles (but it’s a different Ray Charles) in this issue: 6 |

|

|

|

|