|

|

| You’re receiving Vested Interest, our newsletter about why the markets are doing what they’re doing (and what you should do about it, which is usually nothing). Get in touch with comments and questions.

|

|

| Issue #5 ⇒ |

March 20, 2026 |

|

|

|

- Nobody knows anything, Strait of Hormuz edition

- You’re paying more for TV, and you appear to be OK with it

- What kind of capital structure is ideal for manufacturing Tootsie Rolls?

- Why so many millionaires feel financially anxious (it rhymes with “schmaffordability”)

|

|

|

|

|

| Getting in the door of today’s real estate market can be a fraught experience. |

|

|

|

| Three numbers that explain the economic moment. |

|

| $5.10 |

|

The average price of a gallon of diesel fuel in the US—its highest level since 2022. (Information in this newsletter was accurate as of the time of writing but is subject to change.) Diesel powers much of the transportation industry, from trains to trucks, and it’s especially subject to price disruption due to the war in Iran because of the specific type of crude oil it’s made from. Its price surge could presage broader inflation as the cost of moving goods around the country goes up, which is one reason why the Fed didn’t lower interest rates this week and isn’t expected to do so until mid-year at the earliest. (Lower interest rates = more borrowing and spending = higher inflation. Also driving continued market volatility: a high reading on the Producer Price Index, which measures wholesale costs.) So long as the Strait of Hormuz is closed to tankers, this is going to be the top business story pretty much everywhere.

|

| |

| 6% |

|

The miniscule odds, according to Polymarket, that at least 50 ships (about half of the usual amount of traffic) will be passing through the Strait daily by the end of March. On the other hand, one major bank wrote this week that it sees an extended Iran conflict and a cessation of hostilities before “Q2” (i.e. the end of March) as “equally likely,” and another predicted earlier this month that the whole thing would be over in five days. We’re not huge believers in prediction-making here, and we document these guesses only to emphasize that everyone involved appears to be in the dark. And to emphasize that risking money right now on the likelihood of any particular economic or geopolitical outcome in the region coming to pass would be, well, risky. |

| |

| $1 trillion

|

|

How much Nvidia projects it will make on sales of its chips between now and the end of 2027, according to CEO Jensen Huang’s remarks at Nvidia’s annual GPU Technology Conference. For context, Nvidia’s total revenue in fiscal 2025 was a mere $216 billion; it’s a sign of how high baseline expectations have gotten for AI revenue that NVDA actually dropped after Huang made the new projection. (Only a trillion?) Other highlights from the gathering, at which Huang spoke for two and a half hours (!), included the debut of a robotic AI Olaf from Frozen and discussions of chips that will do AI in space. Still, old tech isn’t entirely dead: After Huang said that copper cables are still important in server racks, makers of newfangled fiber-optic cables—which have been in use since 1977—saw their share prices slump. |

|

|

|

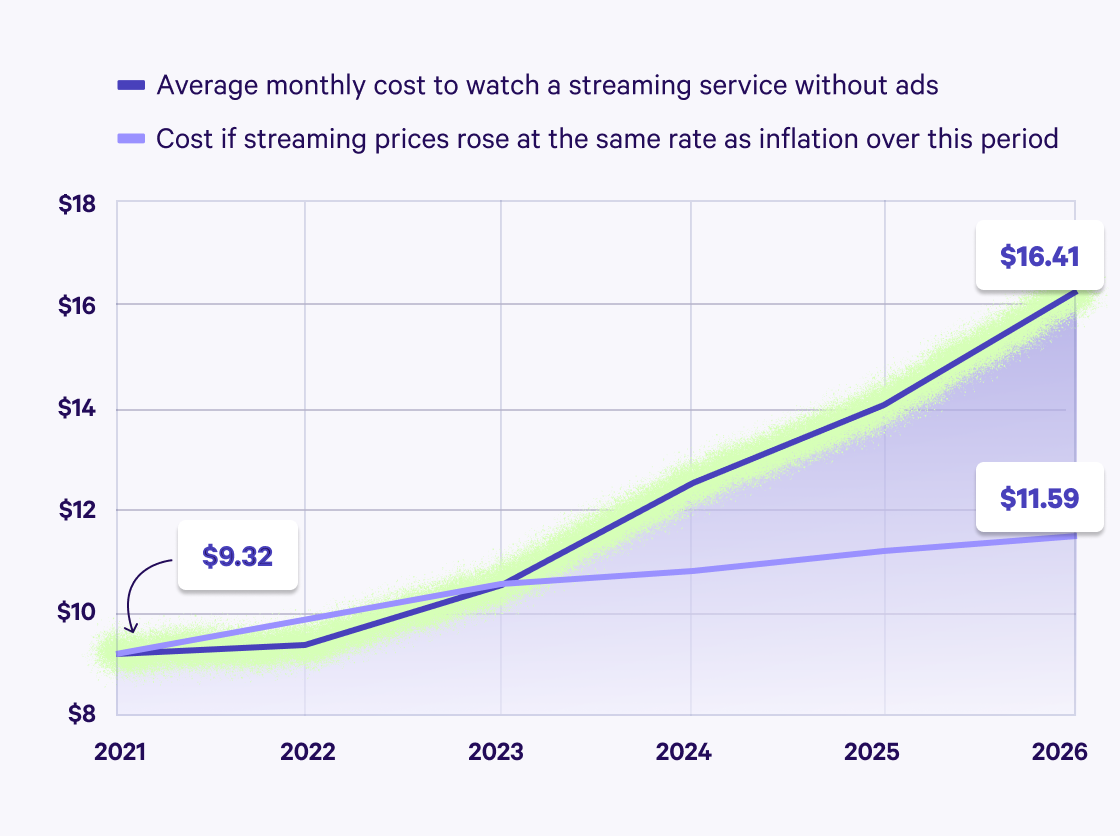

| Streaming services discover the classic business technique of charging more |

|

|

| Includes Netflix, HBO Max, Disney+, Paramount Plus, Apple TV, and Peacock prices for least-expensive no-advertising tier. |

|

The competition to see which media giant will get to own the streaming rights to Warner Bros. properties appears to be over, pending regulatory approval, with Paramount having outbid Netflix. (The plan is to combine Paramount Plus and HBO Max into a single app.) Though it was a notoriously money-losing business for years, streaming can be a profitable enterprise these days thanks in part to the discovery that viewers will accept frequent price increases, advertising interruptions, or both. That said, markets are skeptical that Paramount’s move is going to end up being a winning one because of the amount of debt involved. (Netflix made $2.8 billion for not buying Warner Bros., and its stock rose in the aftermath of the news.)

|

|

|

|

| It may surprise you—okay, it surprised us—that these brands exist as stand-alone companies |

|

|

|

| Third-party logos and trademarks belong to their respective owners; no affiliation or endorsement is implied. Securities shown are for informational purposes only, not a recommendation to buy or hold. |

|

|

The 1960s are known as the golden age of corporate conglomerates in the US, but it’s still rare to see an entire publicly traded company defined by a single brand like the ones above. Should you be so inclined, you could buy stock in Tootsie Roll Industries or Crocs! (The four firms do have other product lines, often added through acquisitions like WD-40’s 1999 purchase of Lava-brand soap.) One outfit that’s no longer on the list is Nathan’s Hot Dogs, bought earlier this year by Smithfield Foods. Bonus investing fact: In 2012, a Journal of Financial Economics article found that the more simple a company’s mission is—the authors actually used the example of a “chocolate producer” in their paper—the faster its stock price tends to adjust to relevant breaking news. (Wealthfront does not encourage speculative day-trading in the chocolate market or any other.)

|

|

|

|

| A lot of millionaires don’t feel wealthy—and the reason why likely matters to you even if you aren’t one of them |

|

|

|

| Jay Gatsby’s combination of property value and anxiety was ahead of its time. (Image via Warner Bros.) |

|

Note: This story has been updated to correct an error regarding the proportion of millennial millionaires.

“Millionaire” is a title that used to automatically signal affluence, but not everyone who qualifies for the designation these days is feeling flush. Last fall, Bloomberg reported that almost one in five U.S. households have a net worth of a million dollars or more—but many still consider themselves “cash-strapped.” In another recent survey, only 36% of respondents with a million-dollar net worth said they felt “wealthy.”

What’s going on? The answer involves the rising costs of housing and other basic needs—and it’s relevant to the financial lives of millionaires, aspiring millionaires, and contended non-millionaires alike.

Housing and other basic expenses are, in fact, historically expensive.

Per Bloomberg, approximately two-thirds of the wealth held by households worth between $1 and $2 million is illiquid, which means it’s tied up in the on-paper value of their homes (or in retirement accounts). Millennials have been accumulating wealth especially quickly, and a 2024 St. Louis Fed report noted that housing assets have driven “the bulk of that growth.” But it’s not just the well-to-do for whom housing has become an unprecedentedly large part of financial life: Home prices relative to wages are historically high up and down the income ladder. Many aspiring home owners have been locked out of the market—researchers at Georgetown found that regulatory changes made in the last decade have substantially tightened access to mortgages, hitting potential first-time buyers the hardest—and rents have risen quickly too. (The reasons why homes have gotten so expensive are hotly debated; for now, let’s just say that many people think it’s largely because there isn’t enough housing to go around.)

But that’s just the start. The prices of groceries and health coverage and child care have been rising faster than the rate of inflation too. Last November, portfolio manager Michael Green went viral with an essay on Substack arguing that the federal poverty line should be raised from $32,150 to $140,000 because of these and other everyday costs. While a lot of economists had technical quibbles with his analysis, he was on to something: There are a lot of all-but-mandatory expenses that go into maintaining a typical standard of living these days.

“What’s happening to a lot of millennials,” economist Kathryn Anne Edwards says, “is they’re facing a steep price tag for normalcy.”

This is a problem—not just for individual households, but potentially for the wider economy.

Even high earners can feel like their economic lives are precarious when so much of their spending and household wealth is tied up in housing. Perma-renters suffer too: According to a recent academic study, there’s a negative correlation between “perceived probability of attaining homeownership” and financially destructive behavior. As people grow more pessimistic about the possibility of owning, that is, they’re more likely to spend less time working, save less money, and make more reckless financial decisions.

What’s more, explains Edwards, the price of housing can hurt the economy overall by eroding the ability to purchase other goods. That danger is the subject of The Land Trap, a recent book by Economist editor Mike Bird. The more valuable property gets in a given country, the more it sucks up attention and resources. Money that would be going into production and consumption, creating growth, gets put instead toward securing housing or speculating in real estate. Among other things, this can lead to bubbles like the one that developed in the US before the 2008 crash.

But you still have choices.

Macroeconomic conditions aside, there are inputs into financial health that individuals have control over. Some parts of the country are less expensive to live in, and some types of jobs are currently more stable and lucrative than others. Finding ways to increase income may be more fruitful than trying to cut costs on mandatory expenses. What not to do, economists and financial professionals tend to agree, is to let the burden or the perceived impossibility of home ownership take such an oversized importance in your mind that it leads you to accrue high-interest debt or neglect the importance of regular old saving and investing.

For one, home values don’t always appreciate at the rate they have in recent years, and are not considered the kind of low-risk asset that can replace retirement savings. As Edwards put it, referring to recent years in which home prices rose by as much as 20% in some markets: “You shouldn’t be making more money on your house than you could investing in the stock market.” Other opportunities for long-run wealth accumulation—like index investing—have historically been lower-risk and provided higher returns than buying property.

Mortgages are sometimes described as a mechanism of “forced savings,” requiring those who hold them to put away a certain amount each month toward home equity. There is also what’s called “consumption value” in home ownership: You can’t settle down for a cozy night making memories with your family in an index fund. Both explain why owning a home is such an important goal for many people. But if you let a disproportionate focus on housing values preclude you from saving and investing for the long run, you might end up as one of those anxious millionaires.

|

|

|

|

|

|

# of mentions of AI in this issue: 3

# of mentions of crypto in this issue: 0

# of mentions of hot dogs in this issue: 1 |

|

|

|

|